By Lance Roberts, Real Investment Advice

With the markets closed yesterday, there is little to update you on with respect to the technical backdrop from this weekend’s missive. However, this is a good opportunity to review the fundamentals as Q2-earnings season comes to a close.

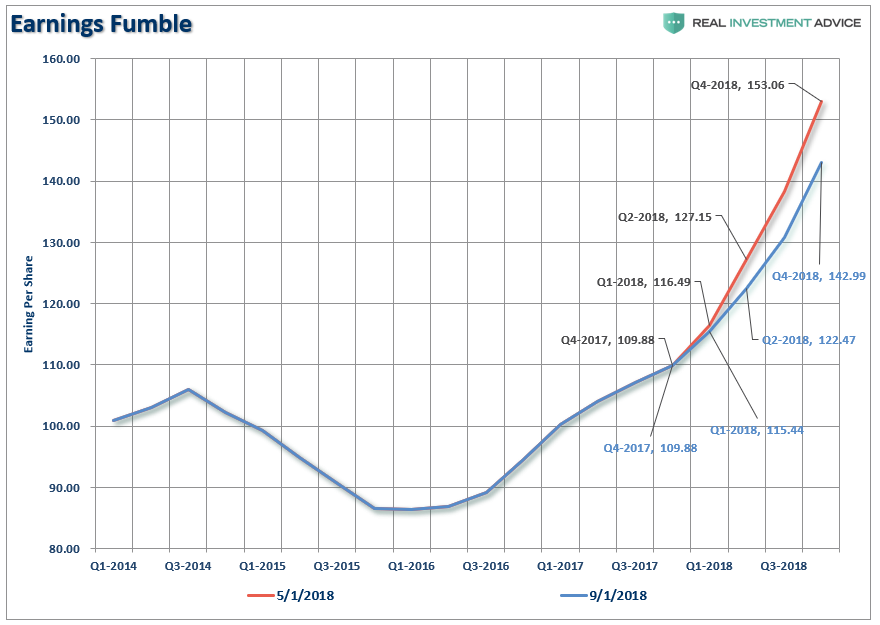

Not surprisingly, the cuts to corporate tax rates in December led to a surge in quarterly earnings numbers. During the first two quarters of this year, 12-month operating earnings per share rose from $124.51 per share in Q4 of 2017 to $132.23 and $140.45 in Q1 and Q2 of 2018 respectively or more than 6% in each quarter. While operating earnings are widely discussed by analysts and the general media; there are many problems with the way in which these earnings are derived due to one-time charges, inclusion/exclusion of material events, and outright manipulation to “beat earnings.”

Therefore, from a historical valuation perspective, reported earnings are much more relevant in determining market over/undervaluation levels. There was good news found here as well with reported earnings also getting a tax-related surge. For the quarter, 12-month reported earnings per share rose from $109.88 in Q4 of 2017 to $115.44 and $122.47 in Q1 and Q2 of 2018 respectively. This also translated into roughly a 6% increase in both quarters.

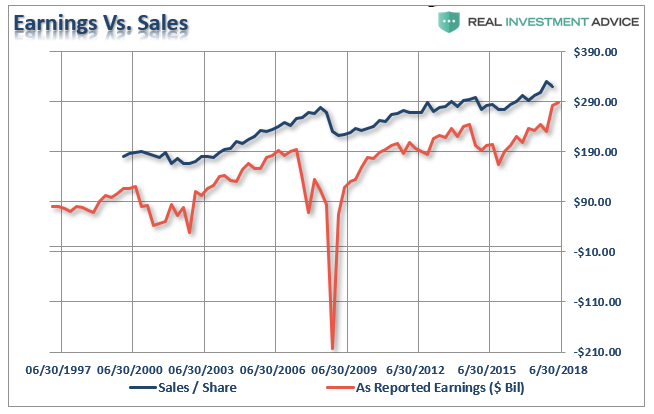

However, despite the improvement in reported earnings for the first quarter, the thing that jumped out was the decline in revenues per share which slumped from $329.59/share in Q4 to $320.39/share in Q1.

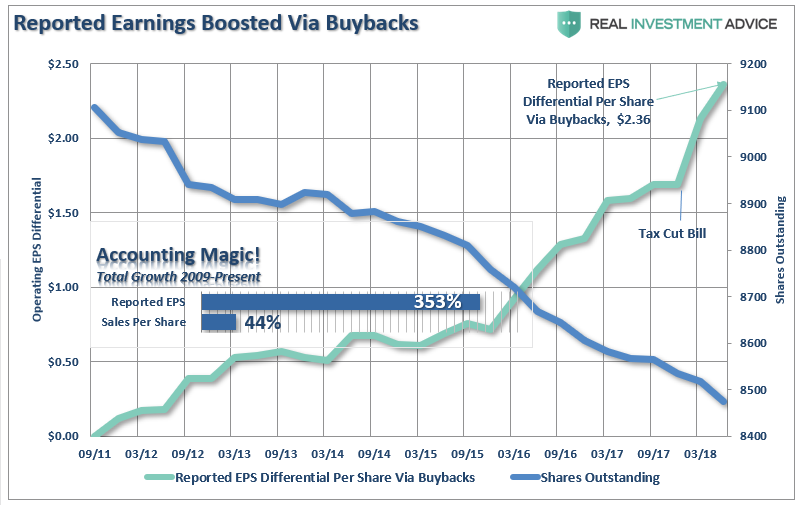

In other words, while top line SALES fell, bottom line revenue expanded as share buybacks and accounting gimmickry escalated for the quarter. The question is whether sales dramatically expanded in Q2? Given some of the recent economic data, we have our doubts and expect a smaller increase. (I will update this chart when S&P updates the sales/share figure for Q2) As shown in the chart below, the biggest support for earnings expansion in Q2 continues to be the dramatic decline in shares outstanding.

Of course, such should not be a surprise. Since the recessionary lows, much of the rise in “profitability” have come from a variety of cost-cutting measures and accounting gimmicks rather than actual increases in top-line revenue. While tax cuts certainly provided the capital for a surge in buybacks, revenue growth, which is directly connected to a consumption-based economy, has remained muted. Since 2009, the reported earnings per share of corporations has increased by a total of 353%. This is the sharpest post-recession rise in reported EPS in history. However, the increase in earnings did not come from a commensurate increase in revenue which has only grown by a marginal 44% during the same period and declined from 49% in Q1.

The reality is that stock buybacks create an illusion of profitability. If a company earns $0.90 per share and has one million shares outstanding – reducing those shares to 900,000 will increase earnings per share to $1.00. No additional revenue was created, no more product was sold, it is simply accounting magic. Such activities do not spur economic growth or generate real wealth for shareholders. However, it does provide the basis for with which to keep Wall Street satisfied and stock option compensated executives happy.

Always Optimistic

But optimism is certainly one commodity that Wall Street always has in abundance. When it comes to earnings expectations, estimates are always higher regardless of the trends of economic data. The problem is that the difference between expectations and reality have been quite dramatic.

Since the beginning of this year, forward expectations have already started falling as economic realities continue to impede overly optimistic projections. However, just since May, estimates for the end of 2018 have fallen by more than $10/share.

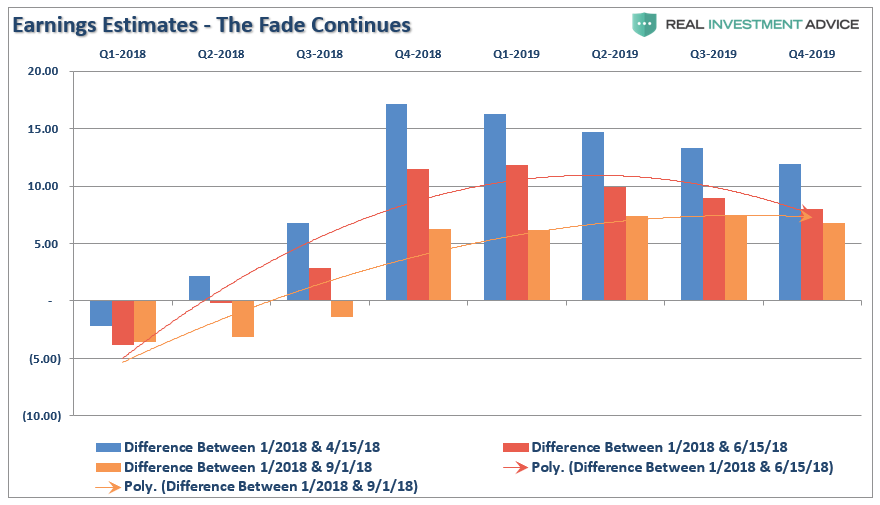

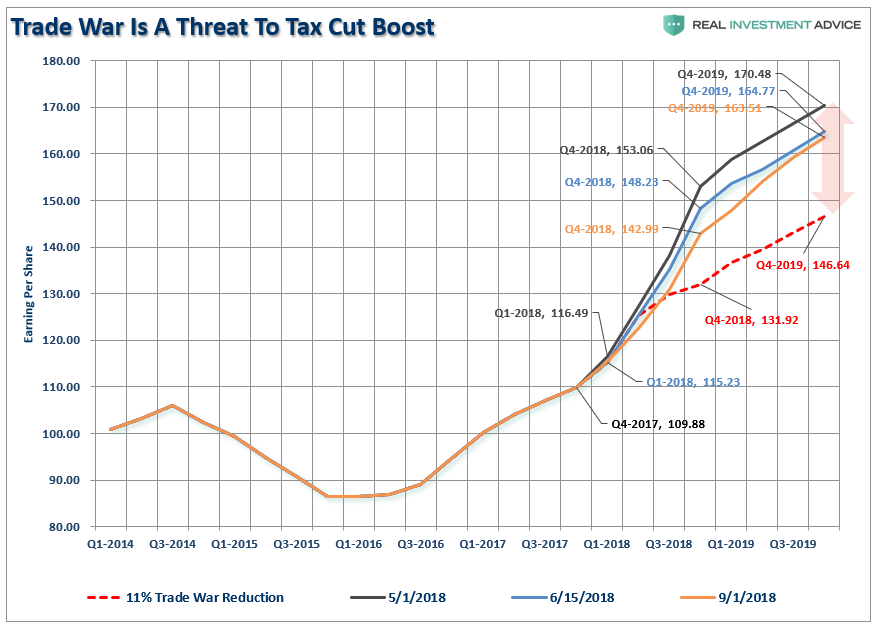

But it isn’t just this year where estimates are falling, but into 2019 as well. The chart below shows the changes in estimates a bit more clearly. It compares where estimates were on January 1st versus April, June and September 1st. Currently, optimism is exceedingly “optimistic” for the end of 2019.

The risk to current estimates going forward remain higher rates, tighter monetary accommodation, and trade wars. As I wrote recently, the estimated reported earnings for the S&P 500 have already started to be revised lower (so we can play the “beat the estimate game”) but an ongoing trade war could effectively wipe out the entire benefit of the tax cut bill. For the end of 2019, forward reported estimates have declined by roughly $9.00 per share.

Comparisons To Get Tougher

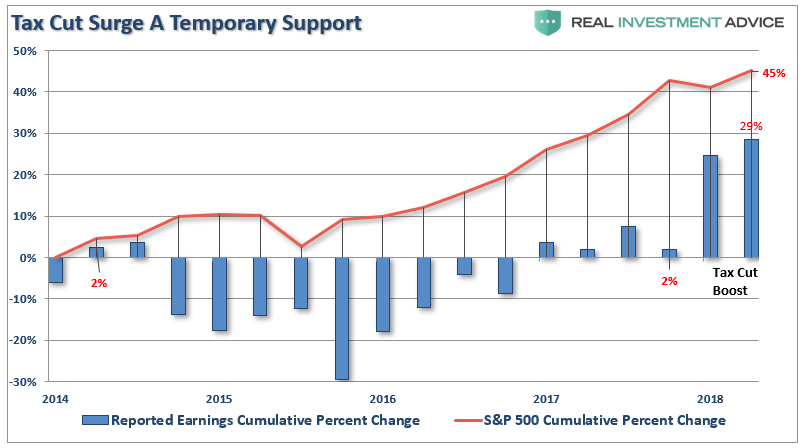

There is no argument that corporate profits have indeed jumped over the last two quarters. The good news is the bump in earnings have helped hold valuations in check. The chart below shows the surge in earnings due to the reduction in corporate taxes.

Notice the stock market rose (capital appreciation only) by over 40% while reported earnings growth rose by a whopping 2% through the end of 2017. However, in the last two quarters, earnings growth has surged by over 20%, but as noted above, that surge came without a commensurate surge in revenues.

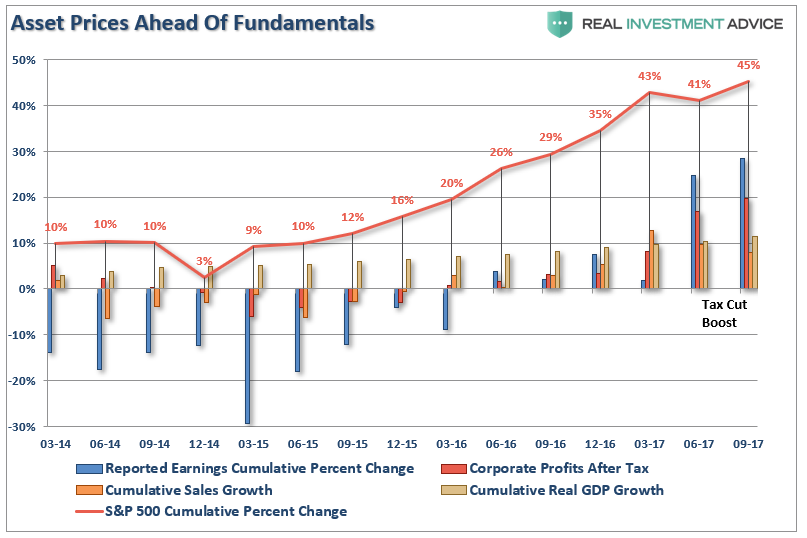

The chart below expands that analysis to include four measures combined: Economic growth, Top-line Sales Growth, Reported Earnings, and Corporate Profits After Tax. Clearly, the stock market has grown substantially faster than all other measures. Since 2014, the economy has only grown by a little more than 10%, top-line revenues by just 9% but corporate profits after tax, and reported earnings, are up over 20%. All of that while asset prices have grown by 45% through Q2.

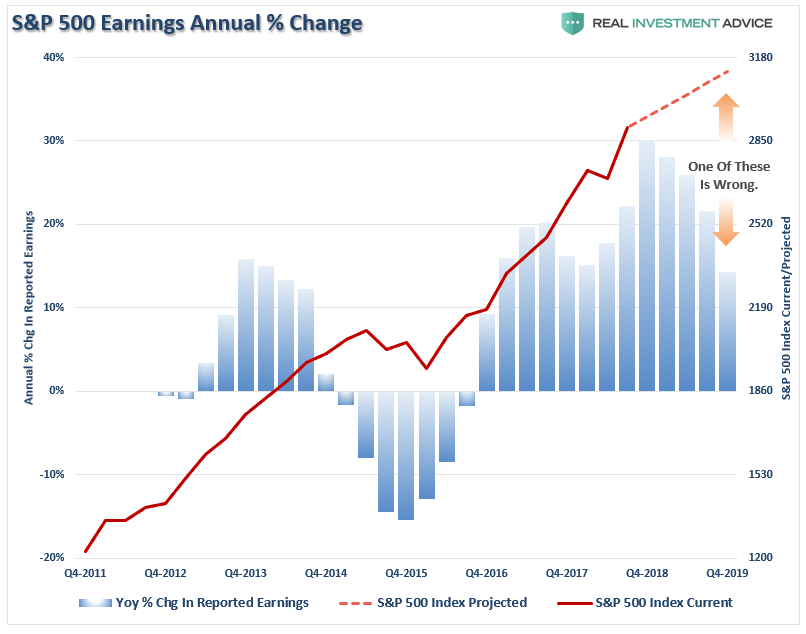

But looking forward, year over year comparisons are going to become markedly more troublesome even as expectations for the S&P 500 index continues to rise.

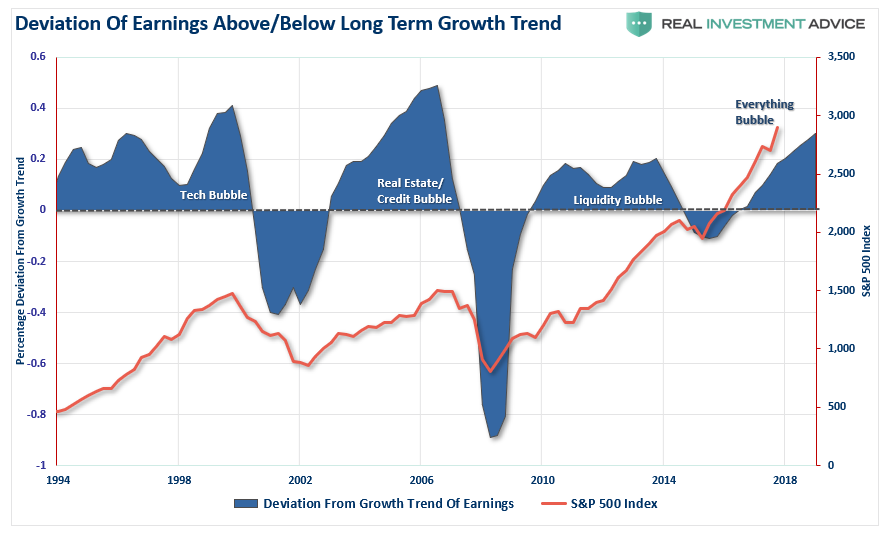

Furthermore, the deviation of earnings from the long-term growth trend are now at levels that have historically denoted reversions as well. Consequently, such reversions have not been kind to stock market investors either.

But despite the data, many on Wall Street are suggesting the recent string of “record highs” is all about improving fundamentals rather than short-term policy-related boosts.

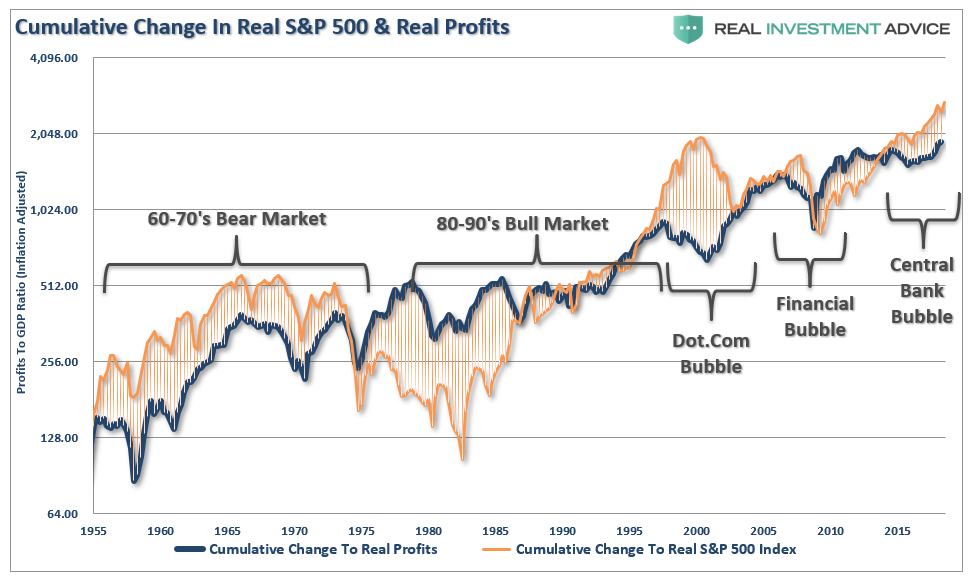

To see if such is indeed the case, we can expand our data back to 1955. The chart below shows the real, inflation-adjusted, profits after-tax versus the cumulative change to the S&P 500. Here is the important point – when markets grow faster than profitability, which it can do for a while, eventually a reversion occurs. This is simply the case that all excesses must eventually be cleared before the next growth cycle can occur. Currently, we are once again trading a fairly substantial premium to corporate profit growth.

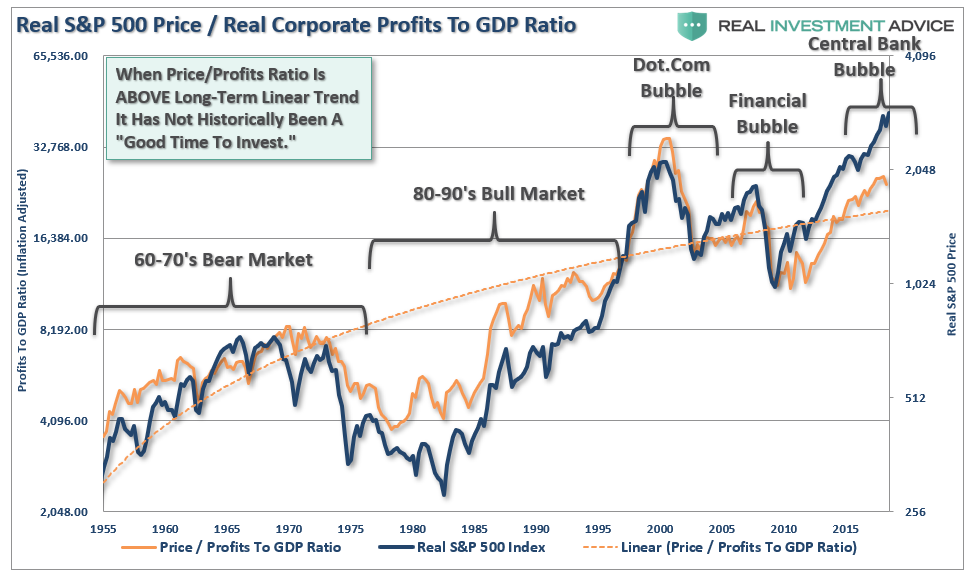

Since corporate profit growth is a function of economic growth longer term, we can also see how “expensive” the market is relative to corporate profit growth as a percentage of economic growth.Once again, we find that when the price to profits ratio is trading ABOVE the long-term linear trend, markets have struggled and ultimately experienced a more severe mean reverting event. With the price to profits ratio once again elevated above the long-term trend, there is little to suggest that markets haven’t already priced in a good bit of future economic and profits growth.

While none of this suggests the market will “crash” tomorrow, it is supportive of the idea that future returns will substantially weaker than in recent years.

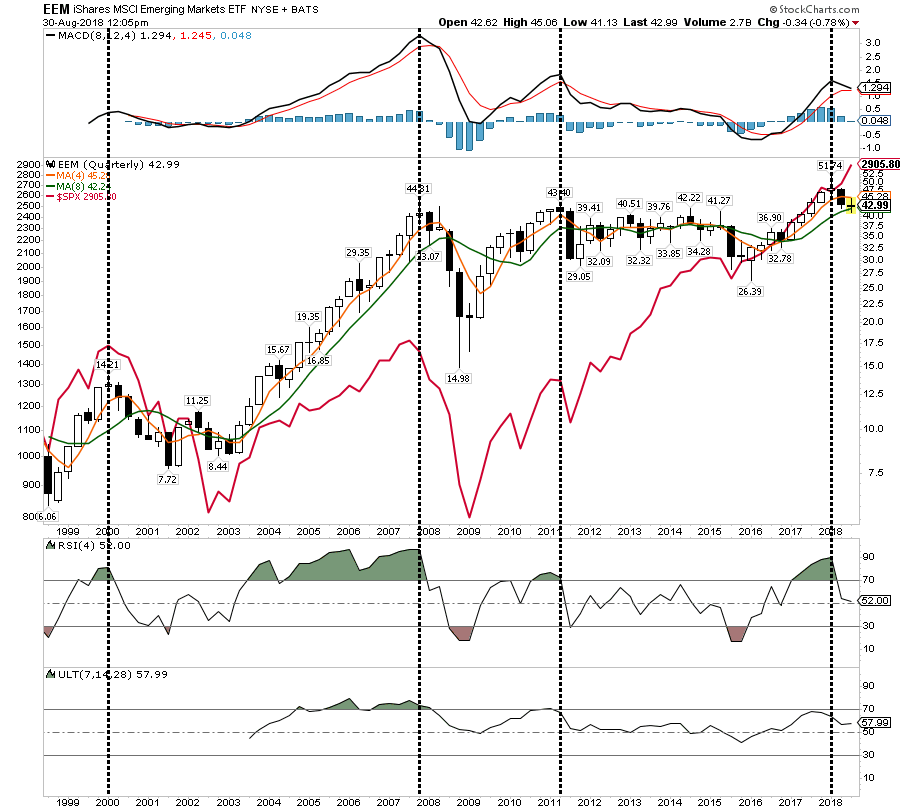

Despite much hope that the current breakout of the markets is the beginning of a new longer-term advancing “bull” market – the economic and fundamental variables suggest otherwise. Also, as I noted last Friday, pay attention closely to the message that emerging markets are sending.

“My position is simply that the economic dependency of emerging markets on the U.S. is extremely high. Therefore, when the U.S. gets a ‘cold,’ emerging markets get the ‘flu.’

Over the last 25-years, this has remained a constant.”

“In 2000, 2007 and 2012, emerging markets warned of an impending recessionary drag in the U.S. (While 2012 wasn’t recognized as a recession, there were many economic similarities to one.)”

With analysts once again hoping for a continued surge in earnings in the months ahead, it is worth noting this has always been the case. Currently, there are few, if any, Wall Street analysts expecting a recession at any point in the future. Unfortunately, it is just a function of time until the recession occurs and earnings fall in tandem.

The deterioration in earnings is something worth watching closely. While earnings have improved in the recent quarter, due to the benefit of tax cuts, it is likely transient given the late stage of the current economic cycle, continued strength in the dollar and potentially weaker commodity prices in the future.

Wall Street is notorious for missing the major turning of the markets and leaving investors scrambling for the exits.

This time will likely be no different.

It is important to remember the bump in earnings growth will only last for one year at which point the analysis will return to more normalized year-over-year comparisons. While anything is certainly possible, the risk of disappointment is extremely high.

It certainly brings to mind Bob Farrell’s Rule #9 which states:

“When all experts agree – something else is bound to happen.”

To access the original article, click here.